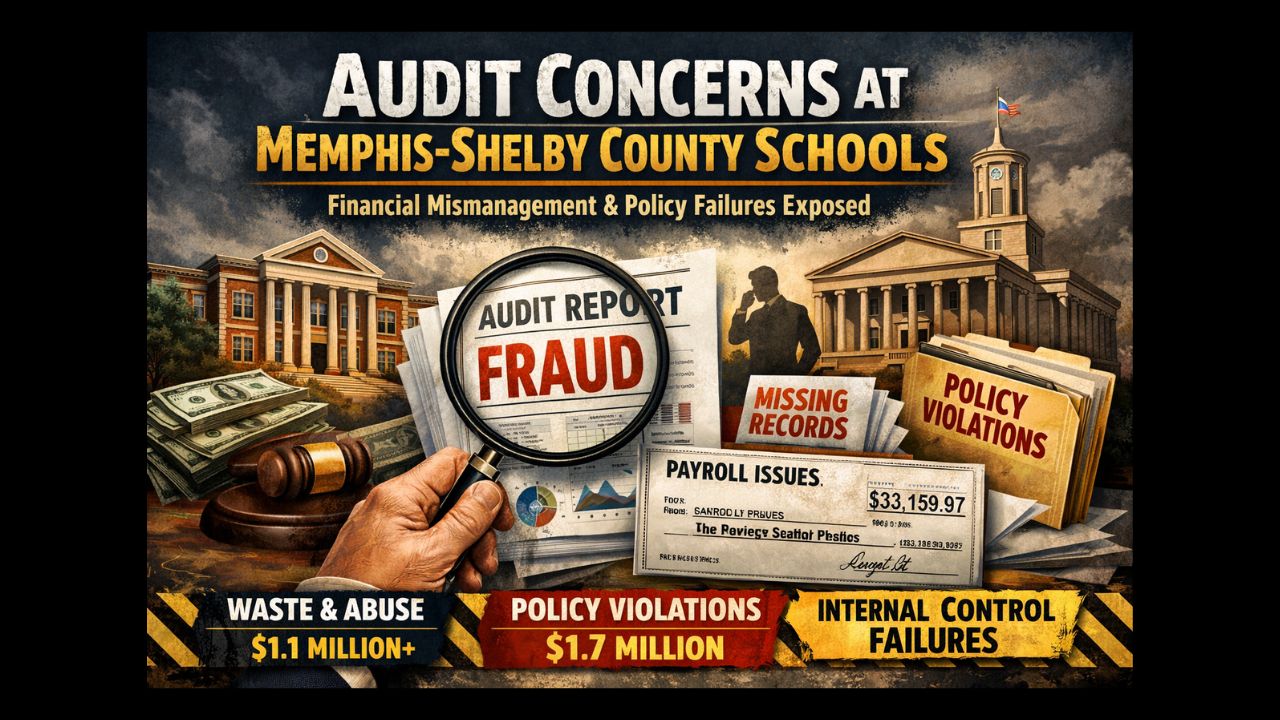

The interim report on the forensic audit of the Memphis-Shelby County Schools (MSCS) has unveiled significant governance and financial management issues, prompting widespread concern among state officials and educators alike.

Commissioned by the Tennessee General Assembly and conducted by Clifton Larson Allen LLP (CLA), the audit covers fiscal years 2022–2024 and aims to uncover potential fraud, waste, and abuse within the state’s largest school district.

On April 1, 2026, state officials, including Tennessee Comptroller Jason Mumpower and House Speaker Cameron Sexton, presented the interim findings, which represent approximately 25% completion of the audit. The full report is expected later in 2026.

Key Findings from the Interim Report

– Deficiencies and Observations: Nearly 175 deficiencies were identified across various sections of the report, indicating systemic issues.

– Financial Mismanagement:

– Disbursements: $1,145,909.97 flagged as waste or abuse, with about $1,112,750 linked to contract-related spending.

– Issues included inadequate oversight, unsupported or duplicative billings, and activity outside procurement controls.

– Payroll Issues: Approximately $33,159.97 in payroll-related transactions, including unsupported vacation payouts, were also noted.

– Policy Violations: An additional $1,729,522.81 in transactions violated district policies but did not reach the level of waste or abuse. These included improperly documented areas such as P-cards and travel reimbursements.

– Internal Control Failures:

– Significant failures in record-keeping, such as the inability to provide employment verification records for 100 out of 250 sampled employees.

– Poorly maintained employee records and fragmented information systems have hindered audit processes.

– Whitehaven STEM Center Investigation: An 85% complete separate investigation noted communication gaps and a lack of formal agreements related to project scope changes.

Comptroller Mumpower characterized the findings as indicative of “clear evidence of management failures” and described the situation as the “worst management [he’s] seen,” highlighting a troubling “culture of apathy and carelessness.”

MSCS leadership, including interim Superintendent Roderick Richmond, pointed out that many of the issues predate the current administration. They emphasized their commitment to transparency and have approved a response plan aimed at addressing the audit’s findings. The district has requested a joint meeting with state officials to discuss the report further.

Lawmakers from both parties are reacting to the findings. Republicans have suggested potential state intervention or legislative measures for enhanced oversight, while Democrats have urged caution, reminding constituents that the interim report reflects only preliminary work.

The audit was prompted by concerns regarding financial management, particularly following the firing of a previous superintendent. Previous routine audits have raised issues such as improper recording of staff changes and continued payments to terminated employees.

As the situation develops, stakeholders are advised to stay updated through the Tennessee Comptroller’s website and MSCS announcements. Media outlets and TriStar Daily are also providing ongoing coverage of the situation.

Contributing Editor JC Bowman, who also serves as the executive director of Professional Educators of Tennessee, stated: “We cannot be mere consumers of good governance; we must be participants. The state was correct to look into the financial situation in Shelby County. My major complaint is that the state is a decade too late.”

For more information, the full interim forensic audit report can be accessed through the Tennessee Comptroller’s website, while MSCS financial reports and related documents are available on their official site.

Author